So, you're ready to open an offshore company and bank account. The first thing to get straight is why you're doing it. An offshore company isn't just another business license; it's a specific legal entity registered in a jurisdiction like the UAE, but it intentionally conducts all its business outside that country. This setup is a game-changer for international entrepreneurs looking for serious tax advantages and asset protection.

Your Guide to UAE Offshore Companies

Setting up a UAE offshore company can feel like navigating a maze, but for entrepreneurs operating on a global scale, it’s an incredibly powerful tool. I'm going to cut through the legal jargon and give you clear, practical insights. We'll break down what a UAE offshore company really is and why so many people use it for tax efficiency and to protect their assets.

At its heart, a UAE offshore company is built for one thing: international business. It's a legal entity registered in the UAE, but it’s strictly forbidden from trading or operating within the local UAE market. That distinction is everything, and it’s what makes it so different from other business setups here.

Distinguishing Offshore from Mainland and Free Zone

Getting the lay of the land is the first step. You have to know the difference between offshore, mainland, and free zone companies to make the right call for your business. Each one is designed for a completely different purpose.

-

Mainland Company: This is your traditional local business. Registered with the Department of Economic Development (DED), a mainland company lets you trade anywhere in the UAE and internationally with no restrictions. If your target customers are in Dubai or Abu Dhabi, this is the way to go.

-

Free Zone Company: A free zone entity gives you 100% foreign ownership and operates inside a specific economic zone. You can trade internationally and within your designated free zone, but to sell directly to customers on the UAE mainland, you'll need a local distributor.

-

Offshore Company: This is a non-resident company, plain and simple. You can't rent an office, sponsor visas for staff, or do any business locally. Its entire purpose is to manage international trade, hold global assets, and handle cross-border payments.

Think of an offshore company as an international business headquarters that’s legally anchored in the UAE for its stability and tax perks, while its actual operations span the globe—never touching the local economy.

Why International Entrepreneurs Choose Offshore Setups

The appeal of a UAE offshore company comes down to a potent mix of financial perks and operational simplicity. If your business has absolutely no connection to the local market, it's a sleek and efficient way to structure your operations.

For years, foreign investors had to weigh the pros and cons of onshore, free zone, and offshore setups carefully. Even with recent laws allowing 100% foreign ownership in many mainland sectors, offshore entities remain the go-to for purely international ventures. Why? Because they completely sidestep the higher costs and regulatory hoops of mainland or free zone registrations.

Just look at the numbers. A mainland setup can run you anywhere from AED 15,000 to AED 50,000+, and free zones range from AED 5,750 to over AED 50,000. Offshore setups are dramatically more cost-effective. For more context on foreign investment rules in the UAE, the analysis on whitecase.com is a great resource.

This cost-efficiency, combined with full profit repatriation and zero corporate tax on foreign income, is what makes the UAE’s offshore jurisdictions a magnet for global entrepreneurs. It's a highly specialized solution built for a business that operates everywhere except the UAE, giving you a secure home base to manage your worldwide interests. By the time you finish this guide, you’ll know exactly how to move forward.

Choosing Between RAK ICC and JAFZA Offshore

When you start looking into setting up an offshore company in the UAE, you’ll quickly discover it’s not a one-size-fits-all situation. The conversation almost always narrows down to two powerhouses: the Ras Al Khaimah International Corporate Centre (RAK ICC) and the Jebel Ali Free Zone Authority (JAFZA) Offshore.

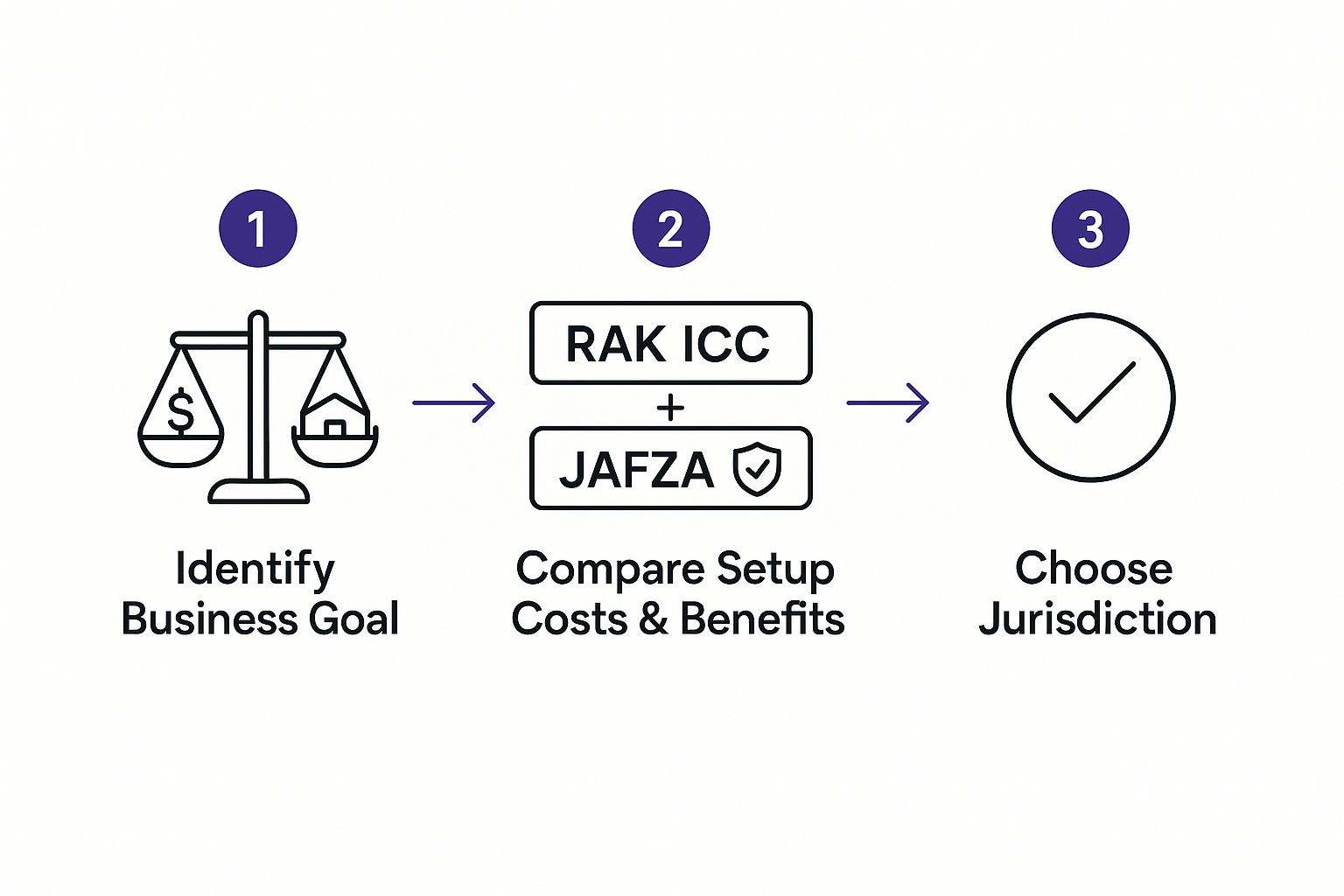

Making the right call isn't about flipping a coin. It’s about matching the jurisdiction to your specific business plan. The best choice for you depends entirely on what you want to achieve. Are you setting up a structure for global trade, or is your main goal to hold real estate in Dubai? The answers to questions like these will point you in a very clear direction.

Align Your Choice with Your Business Goals

The very first question to ask yourself is: what is this offshore company actually for? Your answer is the most important factor in deciding between RAK ICC and JAFZA.

For example, if your primary goal is owning real estate in Dubai, the choice is pretty much made for you. JAFZA Offshore is the only offshore authority that the Dubai Land Department explicitly greenlights for this purpose. If you try to use a different offshore structure, you're just setting yourself up for a world of legal and administrative headaches.

On the flip side, if your business is centered around international trade, asset protection, or holding intellectual property, RAK ICC often comes out on top. It’s a more flexible and cost-effective option built for global business, offering a modern legal framework that isn't tied to a specific local asset like Dubai property.

The process flow below helps visualize how your business needs should guide your decision.

As you can see, it all comes back to your core business activity. That’s the true north when navigating your options.

RAK ICC vs JAFZA Offshore At a Glance

To make the comparison even clearer, here's a direct look at how the UAE's top two offshore jurisdictions stack up. This table should help you quickly identify the best fit for your international business needs.

| Feature | RAK ICC (Ras Al Khaimah) | JAFZA Offshore (Dubai) |

|---|---|---|

| Primary Use Case | International trade, asset protection, holding companies, IP | Holding Dubai real estate, high-value asset holding |

| Cost-Effectiveness | Generally lower setup and annual renewal fees | Higher initial and ongoing costs |

| Reputation | Modern, flexible, and globally respected | Premium reputation, closely associated with Dubai's brand |

| Dubai Property Ownership | Not approved by Dubai Land Department | The only approved offshore authority for holding Dubai property |

| Banking Ease | Widely accepted by UAE banks for international business | Strong relationships with Dubai-based banks |

| Flexibility | High; ideal for a wide range of global business activities | More specialized, primarily for Dubai-centric assets |

Ultimately, RAK ICC is the go-to for entrepreneurs looking for an efficient, affordable global business structure, while JAFZA is the specialist choice for those with a direct investment focus in Dubai.

Comparing Costs and Banking Realities

Money talks, and here, the two jurisdictions speak very different languages. RAK ICC is well-known for its competitive setup and annual renewal fees. This makes it a fantastic choice for entrepreneurs and small to medium-sized businesses who need a solid legal framework without the premium price tag that comes with a Dubai-based authority like JAFZA.

The UAE has been a major player in the offshore world since the 1980s, and jurisdictions like these have perfected the process. You can often get incorporated in less than a week with 100% foreign ownership. Today, you can expect setup costs to fall somewhere between AED 12,500 and AED 20,000. Remember, these companies can’t do business within the UAE, but they're perfect for global activities. The combination of zero corporate tax on foreign income, strong privacy laws, and a pro-business environment keeps driving the sector's growth. You can find more details about the growth of Dubai's offshore sector on binderr.com.

Of course, a company is useless without a bank account. This is the final and most critical step. While banks in the UAE know and respect both jurisdictions, the experience can be different.

-

For RAK ICC: Banks are very comfortable with RAK ICC companies set up for international trade or as holding structures. As long as you have a solid business plan and can show proof of your global operations, the due diligence process is typically smooth.

-

For JAFZA Offshore: Thanks to its connection to Dubai and the massive Jebel Ali Free Zone, a JAFZA company carries a certain prestige. This can sometimes make opening an account, especially with Dubai-based banks, a bit easier. But you have to ask yourself if that slight edge is worth the higher cost, especially if your business has no real link to Dubai.

Your choice sends a signal. A RAK ICC company says you're focused on agile, cost-effective international business. A JAFZA Offshore company, on the other hand, often points to a direct connection with Dubai, especially in real estate. Once you grasp these fundamental differences, you can pick the jurisdiction that truly supports your long-term vision.

Breaking Down the Offshore Company Formation Process

So, how does an offshore company actually come to life? Let's walk through the process from start to finish. I'm going to skip the dense legal jargon and give you a practical, real-world guide on what to expect.

The whole thing boils down to providing clear, verifiable information to the official registrar. Think of it less like navigating a bureaucratic maze and more like laying a solid legal foundation for your global business. Getting this part right from the get-go is the first critical step to successfully open an offshore company and bank account.

Getting Your Paperwork in Order

Before anything else, you need to pull together a file of personal and business documents. This is where most delays happen, but you can sidestep the frustration by getting everything ready ahead of time. Trust me, being organized now will save you weeks of back-and-forth later.

The registrar needs to confirm who you are and where you live. This isn't just red tape; it's a fundamental part of global anti-money laundering (AML) and compliance regulations.

Here’s the essential checklist:

- Certified Passport Copy: This isn't a simple photocopy from your home printer. You'll need to get a lawyer or a notary public to officially stamp and certify that the copy is a true likeness of your original passport. This is a common stumbling block, so make sure it's done right.

- Proof of Residential Address: A recent utility bill (electricity, water, etc.) or a bank statement works perfectly. The key is that it must be dated within the last three months and clearly show both your full name and current address.

- A Simple Business Plan: Don't overthink this. You're not writing a novel. A concise, one-page document is all you need. Just outline your company's planned activities, its target markets (remember, outside the UAE), and where you expect its funds to come from. Honesty and clarity are what matter most here.

The Crucial Role of Your Registered Agent

Here’s a non-negotiable part of the process: you can't form an offshore company by yourself. You absolutely must work through a licensed and approved registered agent. This agent is your official bridge to the offshore authority, whether it's RAK ICC or JAFZA. They handle the document submissions, file the paperwork, and ensure your entire application is compliant.

Choosing the right agent is probably the single most important decision you'll make in this journey. A good one will spot potential issues with your documents before they're even submitted, saving you the headache of rejection. They are your guide and your advocate.

Your registered agent is more than just a setup service; they become your company's official point of contact in the jurisdiction. They are legally responsible for maintaining your company records and ensuring you meet your annual compliance duties, making them a vital long-term partner.

Drafting Your Company's Legal DNA

Once your personal documents get the green light, it's time to create the company's constitutional documents: the Memorandum of Association (MOA) and the Articles of Association (AOA). They sound complex, but your registered agent drafts these for you based on the information you provide.

The MOA basically states what the company is being formed to do. The AOA, on the other hand, lays out the internal rulebook—shareholder rights, how directors are appointed, and procedures for meetings. For most standard offshore companies, these documents are fairly straightforward.

Your input at this stage is simple. You just need to provide:

- Your Proposed Company Name: It’s smart to have three options ready, just in case your top pick is already taken.

- Shareholder Information: Who will own the company? What's the ownership split?

- Director Information: Who will be appointed to manage the company's day-to-day affairs?

Your agent takes this information and weaves it into the formal MOA and AOA, which are then prepared for submission.

From Submission to Your Incorporation Certificate

With a complete application package signed and ready, your agent submits it to the relevant offshore authority. This kicks off the registrar's internal due diligence. They'll verify your identity, review your business plan, and double-check that your company structure ticks all the regulatory boxes.

So, how long does it take? If all your paperwork is in perfect order, you can generally expect to receive your official Certificate of Incorporation within 3 to 5 business days. This certificate is the birth certificate of your company—the legal proof that it exists.

Along with it, you'll get your officially stamped MOA and AOA. These three documents are your "company kit," and they are essential for the next big step: opening your corporate bank account. Guard them carefully, as you'll need certified copies for just about every official transaction your company makes.

Successfully Opening Your Corporate Bank Account

You’ve got your new Certificate of Incorporation in hand—a huge milestone, for sure. But this is really only half the journey. Now comes what is often the most demanding part of the process: actually opening your offshore company’s bank account.

Simply having a registered company doesn't automatically unlock banking services. Your next job is to prove to the bank that your business is legitimate, transparent, and a low-risk client. This is where the real work begins. The process requires careful preparation and an insider's understanding of what UAE banks are actually looking for. They aren't just ticking boxes; they're conducting serious due diligence to protect themselves and the integrity of the entire financial system.

What Banks Really Want to See

When a UAE bank looks at an application from an offshore company, its one and only focus is risk assessment. Their main goal is to avoid onboarding a client that could expose them to financial crime, regulatory fines, or reputational damage. A huge piece of this is navigating anti-money laundering (AML) regulations, which form the bedrock of international banking compliance.

To get your application across the finish line, you have to present a business case that is both compelling and completely credible. This means providing clear, verifiable evidence that directly addresses their biggest concerns.

Here’s what they’re zeroing in on:

- A Credible Business Model: Your business plan needs to be clear, logical, and full of detail. Explain exactly what your company does, who your clients are, and which markets you serve. Vague, generic descriptions like "general trading" or "consulting" are immediate red flags that can get your application tossed.

- Proof of Economic Substance: Banks need to see that you’re running a real business, not just a paper company. You can show this with things like signed contracts, supplier invoices, client agreements, or even a professionally built business website.

- Clear Source of Funds: You must be able to clearly explain where your initial business capital is coming from and back it up with documentation. This is an absolutely non-negotiable part of their Know Your Customer (KYC) process.

I’ve seen so many people make the mistake of treating the bank account application like a simple formality. It’s not. It’s a pitch. You are selling the bank on the legitimacy of your business, and your documents are your sales pitch. Make them professional, thorough, and crystal clear.

Preparing a Compelling Company Profile

Think of your application package as a complete company profile. This is your opportunity to tell your business's story in a way that builds trust and satisfies the bank's compliance team from the get-go. A well-prepared profile anticipates their questions and provides the answers before they even have to ask.

Your package should include all the standard corporate documents, of course, but it needs more than that. Add a detailed business write-up that covers your own professional background, your experience in the industry, and a full picture of how your business operates. The more professional and transparent your presentation is, the better your chances are for a smooth and quick approval.

Traditional vs. Digital Banks

The banking world has changed, and you now have more options than ever. For an offshore company, the choice often boils down to a classic brick-and-mortar bank or one of the newer digital banking platforms.

- Traditional Banks (e.g., Emirates NBD, RAKBANK): These are the established players. They offer a full suite of services, from trade finance and credit lines to dedicated relationship managers. Their global recognition adds a layer of prestige. The trade-off? Their due diligence is often tougher, and they almost always require you to show up for an in-person meeting. Minimum deposit requirements can also be higher, frequently starting at AED 25,000 or more.

- Digital Banks and Fintechs (e.g., Wio Bank): These platforms offer a more modern and streamlined experience, often with lower fees and no minimum balance rules. While you can sometimes get onboarded remotely, their services can be more limited compared to the big banks. They are a fantastic choice for businesses that just need straightforward international payments and currency management.

The best option really depends on what your business needs. If you require complex financial tools like letters of credit, a traditional bank is probably your only choice. If your top priority is fast, affordable global transactions, a digital bank could be the perfect fit.

The In-Person Visit and Realistic Timelines

While you can handle much of the company formation process from your home country, you should absolutely plan on visiting the UAE to finalize the bank account. For nearly all traditional banks, a face-to-face meeting with the primary shareholder or account signatory is a mandatory compliance step. This is their chance to verify your identity in person and ask any final due diligence questions.

Finally, be realistic about how long this takes. Opening a corporate bank account for an offshore company isn't an overnight affair. From the day you submit your complete application, you should expect it to take anywhere from two to six weeks for the bank to complete its internal reviews and give you your account details. It’s crucial to factor this waiting period into your business plan to keep your operations running smoothly.

Staying Compliant After Your Company Is Formed

Getting your company registered and the bank account open are huge first steps, but the work doesn't stop there. It's one thing to successfully open an offshore company and bank account; it’s another thing entirely to keep it in good standing for the long haul. This isn't just about ticking boxes—ongoing compliance is what protects the value and integrity of your entire setup.

I like to think of a new company like a brand-new car. The setup process is you buying the car off the lot. The ongoing compliance? That's the regular maintenance that keeps it running smoothly and, most importantly, legally. If you skip the oil changes and tune-ups, you're asking for trouble. It's the same here—neglecting these simple but critical steps can lead to hefty penalties, a frozen bank account, or even the jurisdiction striking your company from the register.

Your Annual Compliance Checklist

Staying compliant is actually pretty straightforward if you're organized. While your registered agent is there to guide you, the ultimate responsibility falls on you, the owner, to make sure everything gets done on time. We're not talking about complicated annual audits for most structures, just a few essential tasks each year.

The absolute number one priority is paying your annual renewal fees to the offshore authority. This is what keeps your company's name on the official register as "active." Missing this deadline is the fastest way to lose your good standing, which immediately puts your bank account and any company contracts at risk.

Your core duties each year really boil down to this:

- Pay Your Renewal Fees on Time: This is non-negotiable. It keeps your company legally alive. I always tell my clients to put this deadline in their calendar with multiple reminders.

- Keep Good Financial Records: Even if your jurisdiction doesn't demand a formal audit, you absolutely must maintain clear records of all income and expenses. This is crucial for your own management and vital if the bank ever asks for an update.

- Maintain Your Registered Agent and Office: You are required to have a registered agent and office in the jurisdiction at all times. The good news is this is typically covered by your annual renewal fee.

Understanding Global Transparency Standards

The offshore world has changed dramatically over the past decade, moving toward much greater transparency. Jurisdictions like the UAE are all-in on meeting global standards set by organizations like the OECD. There are two key sets of rules you need to have on your radar: Economic Substance Regulations (ESR) and Ultimate Beneficial Ownership (UBO).

These aren't just local quirks; they are part of a massive global push to make sure offshore companies are used for legitimate business, not for stashing illicit cash. Proactive compliance is your best defense and shows you're running a credible, transparent international operation.

Ultimate Beneficial Ownership (UBO) rules simply mean you have to declare who the real, human owners of the company are. This information is held securely by the authorities—it's not public—but it provides a clear line of sight for regulators.

Economic Substance Regulations (ESR) come into play if your company is involved in specific activities like banking, insurance, or holding intellectual property. You might need to show that the company has real economic activity in its home jurisdiction, which could mean having employees or physical office space there. Your agent can tell you right away if this applies to your business.

Protecting Your Long-Term Integrity

Staying compliant is about so much more than just avoiding fines. It's about future-proofing your business. Banks are under incredible pressure to make sure their clients are playing by the rules. Staying on top of things like Anti-Money Laundering (AML) compliance is absolutely essential for any offshore company today. From the bank's perspective, a company with a perfect compliance history is a low-risk, high-quality client.

This simple fact makes it infinitely easier to maintain your current banking relationships and open new ones down the road. By diligently handling your annual tasks, you ensure your offshore company remains a powerful and respected tool to achieve your international goals for years to come.

Your Top Questions About UAE Offshore Companies

When you're exploring setting up a business overseas, questions are bound to pop up. It's only natural. Getting straight answers is the only way to move forward with confidence, especially when you plan to open an offshore company and bank account.

Let's tackle some of the most common questions we hear from international entrepreneurs. This should help clear up any lingering confusion about what a UAE offshore company can—and can't—do for you.

Can I Get a UAE Residency Visa with an Offshore Company?

This is probably the biggest misconception out there, so let’s get right to the point: No, a UAE offshore company does not grant you a residency visa.

This type of company is designed purely for international business and asset holding, all conducted outside the UAE. Since you can't rent an office or hire staff locally, there's simply no mechanism for visa sponsorship. If a UAE visa is one of your main goals, you'll need to look at setting up in a free zone or on the mainland.

What's the Real Difference Between an Offshore and a Free Zone Company?

The core difference is where you can legally do business. An offshore company is a non-resident entity, a legal tool built for international trade and holding assets around the world. It is strictly prohibited from doing any business inside the UAE.

A free zone company, however, gives you much more operational freedom. With a free zone setup, you can:

- Trade internationally without any issues.

- Do business within your specific free zone.

- Rent a physical office.

- Sponsor UAE residency visas for yourself and your employees.

Both structures give you 100% foreign ownership, but a free zone company provides a genuine physical presence in the UAE. An offshore company, in contrast, is simply a legal and financial vehicle for your global activities.

Here's a simple way to think about it: An offshore company is your international HQ, legally based in the UAE for its tax and legal benefits. A free zone company is your actual operational base on the ground in the UAE, ready to serve both local and global clients from its specific zone.

Do I Have to Fly to the UAE to Open the Bank Account?

For the most part, yes, a personal visit is non-negotiable. While we can handle the entire company formation process for you remotely, UAE banks are incredibly strict with their Know Your Customer (KYC) and compliance checks.

At least one shareholder or signatory will need to show up in person for a final meeting with the bank. It's a key step they take to prevent fraud. While some newer digital banks are starting to offer remote options, this isn't the norm for the major, established banks, especially when dealing with offshore clients. You absolutely need to factor a trip into your timeline and budget.

Will I Have to Pay UAE Corporate Tax on My Offshore Company?

This is one of the biggest draws. A UAE offshore company is generally not subject to corporate tax on income earned from activities outside the UAE. That tax efficiency is precisely why so many entrepreneurs use this structure for their global businesses.

But—and this is a big but—that tax exemption only applies within the UAE. You are still fully responsible for any personal and corporate taxes in your home country. Tax laws change, so it's always smart to get advice from a qualified tax professional to make sure your setup is 100% compliant everywhere.

✅ Best Corporate Service Provider in Dubai, Abu Dhabi & Sharjah

✅ Specialists in Mainland Company Formation in Dubai & Abu Dhabi

✅ Specialists in Freezone Company Formation across the UAE

✅ 24/7 Support Service – Always here when you need us

✅ Cost-Effective Business Setup Solutions tailored to your needs

✅ Enjoy UAE Tax Benefits for International Entrepreneurs

📞 Call Us Now: +971-52 923 1246

💬 WhatsApp Us Today for a Free Consultation